Antwort What is the biggest difference between IFRS and GAAP? Weitere Antworten – What is the major difference between GAAP and IFRS

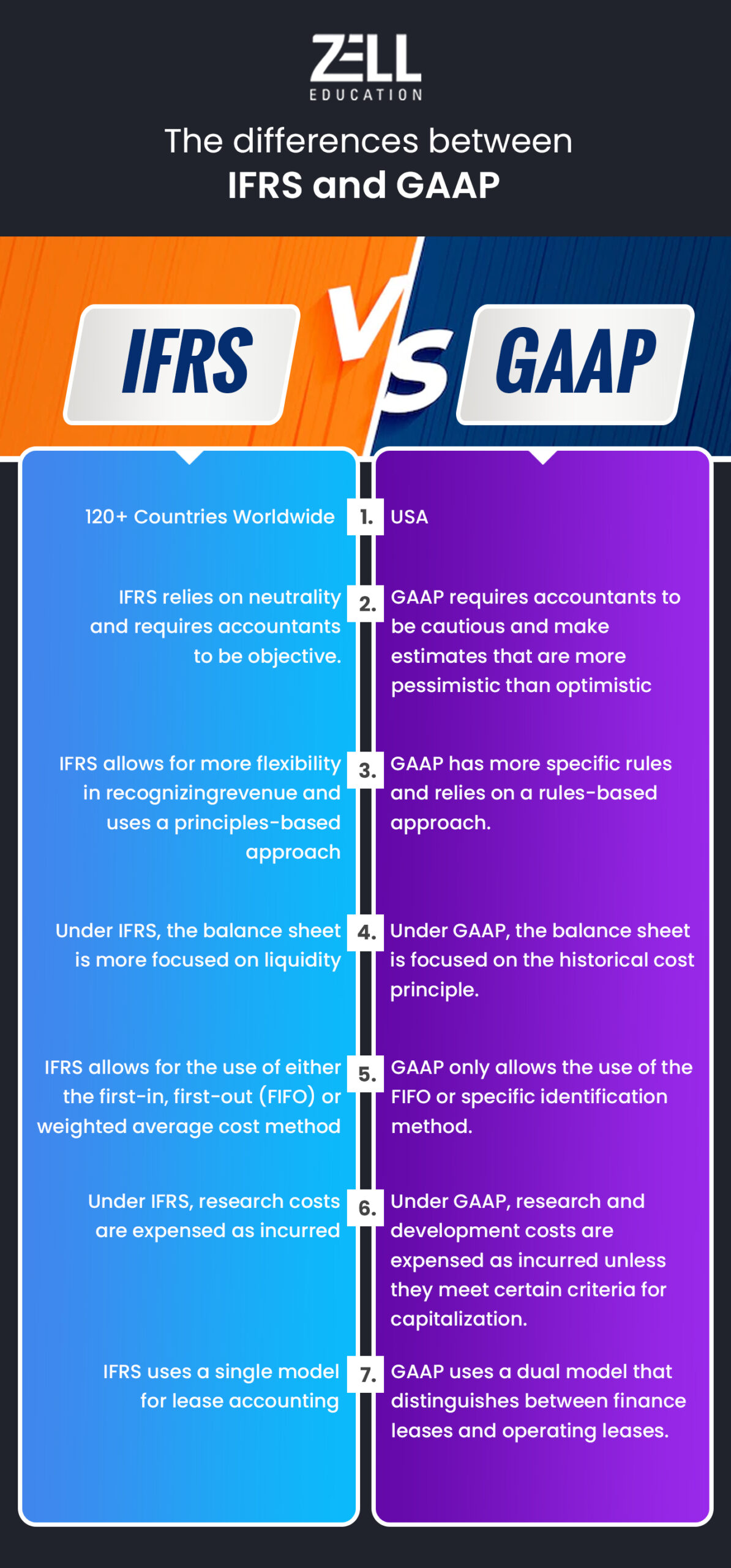

IFRS stands for International Financial Reporting Standards, which are a set of internationally accepted accounting standards used by most of the world's countries. The key differences between GAAP and IFRS include: GAAP is a framework based on legal authority while IFRS is based on a principles-based approach.US GAAP lists assets in decreasing order of liquidity (i.e. current assets before non-current assets), whereas IFRS reports assets in increasing order of liquidity (i.e. non-current assets before current assets).IFRS: use method that matches the actual flow of goods. LIFO is prohibited. US GAAP: use method that most clearly reflects periodic income.

What is the advantage of IFRS over GAAP : Key Takeaways. Under GAAP, once inventory has been written down, any reversal is prohibited. Under IFRS, a write-down of inventory can be reversed in future periods if specific criteria are met. The move to a single method of inventory costing could lead to enhanced comparability between countries.

Is IFRS more strict than GAAP

IFRS is principles-based, whereas GAAP is rules-based. Essentially, this means that GAAP is far stricter than IFRS, offering specific rules and procedures that leave little room for interpretation. By contrast, IFRS provides general guidelines that companies are encouraged to interpret to the best of their ability.

What are the four basic GAAP principles : The most notable principles include the revenue recognition principle, matching principle, materiality principle, and consistency principle. Completeness is ensured by the materiality principle, as all material transactions should be accounted for in the financial statements.

One of the most basic differences is that GAAP permits the use of all three of the most common methods for inventory accountability—weighted-average cost method; first in, first out (FIFO); and last in, first out (LIFO)—while the IFRS forbids the use of the LIFO method.

IFRS: Requires disclosure of material judgments/estimates made in applying accounting policies. Generally made in Summary of Significant Accounting Policies. US GAAP: Requires disclosure of estimates, but not judgments.

What are the weaknesses of IFRS

An especially troublesome weakness of IFRS is that it does not necessarily utilize possible built-in crosschecks. Thus, for example, a reported IFRS “income” number may easily be in conflict with other figures in the same financial period.Essentially, this means that GAAP is far stricter than IFRS, offering specific rules and procedures that leave little room for interpretation. By contrast, IFRS provides general guidelines that companies are encouraged to interpret to the best of their ability.GAAP permits the use of all three of the most common methods for inventory accountability; the IFRS forbids the use of the LIFO method. IFRS requires that inventory is carried at the lower of cost or net realizable value; U.S. GAAP requires that inventory is carried at the lower of cost or market value.

GAAP (generally accepted accounting principles) is a collection of commonly followed accounting rules and standards for financial reporting. The acronym is pronounced gap. GAAP specifications include definitions of concepts and principles, as well as industry-specific rules.

What is the main goal of GAAP : GAAP sets out to standardize the classifications, assumptions and procedures used in accounting in industries across the US. The purpose is to provide clear, consistent and comparable information on organizations financials.

What are 2 key similarities between US GAAP and IFRS : How are GAAP and IFRS similar Despite several differences, there are some similarities between IFRS and GAAP. These include the use of a balance sheet, cash flow statements, and income statements. Both principles offer the same functionality to organizations dealing with cash and cash equivalent.

What is the major difference between US GAAP and IFRS affecting the lease accounting practice

Another key difference between IFRS Standards and US GAAP relates to the treatment of leases whose payments depend on an index or rate – e.g. a lease with payments adjusted annually for changes in the consumer price index (CPI). Under IFRS 16, the lease liability is remeasured each year to reflect current CPI.

Essentially, IFRS is based on the guiding principle that revenue is recognized when value is delivered. GAAP has much more specific rules regarding how revenue is recognized in different industries, but essentially, income isn't recognized until goods have been delivered or a service has been rendered.Disadvantages of IFRS include a lack of detail, significant adoption costs, and the perception that IFRS is a less stringent standard than what is already in place in some countries.

What are the problems between GAAP and IFRS : Key Differences

IFRS guidelines provide much less overall detail than GAAP. Consequently, the theoretical framework and principles of the IFRS leave more room for interpretation and may often require lengthy disclosures on financial statements.